Introduction

Many property owners hear "cost segregation study" and immediately wonder whether the upfront fee — often several thousand to tens of thousands of dollars — is worth it. That hesitation is understandable. For the right property, cost segregation ROI isn't speculative — it's calculable before you spend a dollar.

Studies routinely generate returns of 10x to 65x the study fee in year one alone — a figure drawn from Seneca Cost Segregation's 10,200+ completed engagements. The math isn't complicated. It just requires knowing which variables drive the outcome.

This article covers:

- How cost segregation ROI is calculated

- Which property scenarios produce the strongest returns

- When a study genuinely doesn't pencil out

- How to quickly assess whether your property qualifies

Key Takeaways

- ROI depends on three factors: depreciable basis, your marginal tax rate, and property type — not just purchase price

- Qualifying properties routinely generate 10–40x returns on study fees in year one

- The One Big Beautiful Bill made 100% bonus depreciation permanent for qualified property placed in service after January 19, 2025

- Low tax brackets, short holding periods, or passive loss limitations can reduce or delay ROI

- Every month without accelerated depreciation is lost savings — and lost compounding on that capital

How Cost Segregation ROI Works: The Math Made Simple

The Depreciation Problem Standard Schedules Create

Under IRS Publication 946, residential rental property depreciates over 27.5 years and commercial property over 39 years. That means a $1.5M building generates roughly $38,000–$54,000 in annual deductions — an amount that does little to offset the capital demands of early ownership.

Cost segregation changes that math by reclassifying components into faster depreciation categories:

- 5-year property: Carpet, appliances, decorative fixtures, specialty flooring, data cabling

- 7-year property: Office furniture, filing systems, certain HVAC equipment

- 15-year property: Parking lots, landscaping, fencing, outdoor lighting, sidewalks

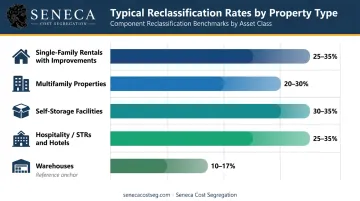

Seneca's engineering team typically reclassifies 10–40% of depreciable basis into these shorter categories, depending on property type. Warehouses sit at the lower end (10–17%), while mobile home parks can reach 80–85% due to their infrastructure composition.

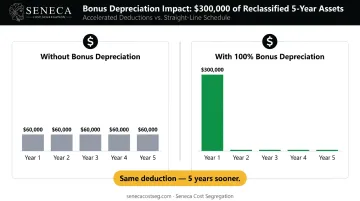

How Bonus Depreciation Amplifies the First-Year Impact

Reclassification alone creates acceleration — but bonus depreciation creates a step-change. For qualified property acquired and placed in service after January 19, 2025, 100% bonus depreciation is now permanent under current law.

Without bonus depreciation, $300,000 of reclassified 5-year assets would generate roughly $60,000 per year in deductions over five years. With 100% bonus depreciation, that same $300,000 is fully deducted in year one — front-loading the tax benefit precisely when capital needs are highest. That timing difference is what makes cost segregation so effective for investors scaling a portfolio.

The ROI Formula in Plain Numbers

Here's how the math works on a hypothetical $1.5M property:

| Variable | Amount |

|---|---|

| Purchase price | $1,500,000 |

| Estimated land value | $300,000 |

| Depreciable basis | $1,200,000 |

| Reclassified basis (25%) | $300,000 |

| Tax bracket | 32% |

| First-year tax savings | $96,000 |

| Estimated study fee | $10,000–$15,000 |

| Return multiple | 6–10x |

At the 37% bracket, those same $300,000 of reclassified deductions produce $111,000 in savings — a higher return on the same study fee.

That return looks even stronger when you see what the study fee actually covers. Seneca's fee includes:

- Full engineering report with photo documentation

- Depreciation schedules and cost reconciliation workpapers

- Form 3115 preparation where needed

- CPA implementation support

- AuditDefense — all at no additional charge

When a Cost Segregation Study Pays for Itself

The Payback Period Concept

A study "pays for itself" the moment first-year tax savings exceed the study fee. For qualifying properties, that threshold is crossed within weeks of filing, often well before the year is out. The key inputs that determine how fast:

1. Depreciable basis (not purchase price) Land is not depreciable. If you paid $2M for a property but $500,000 is land, your depreciable basis is $1.5M. The ratio of improvements to total purchase price drives every downstream number in the ROI calculation.

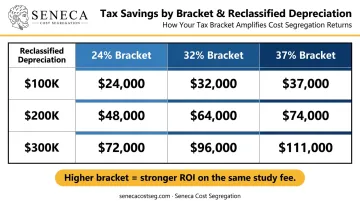

2. Tax bracket multiplier Every dollar of reclassified depreciation saves you exactly your marginal rate in taxes. The difference across brackets is substantial:

| Reclassified Depreciation | 24% Bracket | 32% Bracket | 37% Bracket |

|---|---|---|---|

| $100,000 | $24,000 | $32,000 | $37,000 |

| $200,000 | $48,000 | $64,000 | $74,000 |

| $300,000 | $72,000 | $96,000 | $111,000 |

3. Passive loss usability This is where many investors hit a snag. If you can't immediately use the losses against active income, ROI gets deferred — the savings don't disappear, they just arrive later.

Real Estate Professional Status (REPS) requires more than 750 hours in real property trades or businesses and more than half of your total personal services time. Meeting REPS and material participation tests allows losses to offset active income immediately, which dramatically accelerates payback.

Seneca's Benchmark

Those three inputs — basis, bracket, and loss usability — are exactly what Seneca's engineering team analyzes before quoting a study. Across 10,200+ completed studies, Seneca's average first-year deduction is $171,243. At a 32% tax bracket, that translates to roughly $54,800 in tax savings in year one. At 37%, it's over $63,000. Study fees for properties at that scale typically run into the low-to-mid five figures — meaning most clients see a 3x to 5x return on the study cost in year one alone.

Property Scenarios That Generate the Strongest ROI

Property type, age, and recent improvements each affect how much basis can be reclassified — making some properties dramatically better candidates than others.

New Purchases and New Construction

Properties placed in service after January 19, 2025 benefit from 100% permanent bonus depreciation — maximum reclassifiable basis, immediate deductions, and no lookback complexity. A 35-unit multifamily development Seneca studied in Albany, Oregon generated $1,250,371 in first-year deductions and $423,006 in tax savings on a $5.89M cost basis — placed in service in 2023, when 80% bonus depreciation applied. With 100% bonus now permanent, comparable properties will yield even stronger results.

Short-Term Rentals and Hotels

STRs and hotels carry high concentrations of personal property — furniture, appliances, electronics, decorative finishes — that qualify for 5-year or 7-year treatment. Hotels are particularly asset-rich: multiply qualifying fixtures across 100+ rooms and the reclassifiable basis accumulates fast. Seneca typically sees 25–35% reclassification rates on hospitality properties.

STR owners carry one more advantage. When average guest stay is 7 days or less, the IRS does not treat the activity as a rental activity under 26 CFR § 1.469-1T — meaning losses may be non-passive if the owner materially participates. That means losses offset ordinary income directly — accelerating payback on study costs.

Multifamily and Commercial Properties with Major Improvements

Capital improvements of $50,000+ create fresh depreciable basis eligible for reclassification — and this applies to existing owners who renovated, not just buyers.

A single-family rental Seneca studied in Las Vegas, purchased for $370,000 with $50,000 in improvements, achieved 33.14% total reclassification — generating $119,377 in first-year deductions and $41,832 in tax savings. The improvement basis pushed reclassification significantly higher than the property would have achieved alone.

Typical reclassification rates by property type:

- Single-family rentals with improvements: 25–35%

- Multifamily properties: 20–30%

- Self-storage facilities: 30–35%

- Hospitality (STRs and hotels): 25–35%

When a Cost Segregation Study Doesn't Make Sense

Not every property qualifies. Three situations consistently produce unfavorable math:

Depreciable basis is too low Seneca applies a practical floor of approximately $300,000–$500,000 in depreciable basis (excluding land). Below that threshold, study fees consume too large a share of potential savings. Third-party sources including Moss Adams and Windes point to $1M+ in building basis as a stronger threshold for maximizing ROI — though meaningful savings are possible at lower values when significant improvements are present.

Tax situation mismatches Investors in the 24% bracket see real savings, though the return multiple is lower. Those below 24% — or with no near-term ability to absorb passive losses — may find that benefits are deferred long enough to undermine the investment case.

Cost segregation works in direct proportion to your tax capacity. Without sufficient taxable income to absorb accelerated deductions, the savings clock doesn't start right away.

Short planned holding period Depreciation recapture applies at 25% on unrecaptured Section 1250 gain when you sell. Investors planning to exit within 2–3 years may find that recapture erodes much of what they saved upfront.

A 5+ year holding period is generally where first-year savings comfortably outweigh eventual recapture liability. Investors rolling proceeds into a new property via a 1031 exchange can defer recapture indefinitely.

The Cost of Waiting: Why Delaying Hurts More Than It Seems

The Compounding Argument

A $100,000 tax savings in year one isn't just $100,000. Reinvested at 7% annually:

- After 5 years: ~$140,255

- After 10 years: ~$196,715

Delay the study by one year and you lose the savings and every dollar of compounding on that capital. For investors running multiple properties, that opportunity cost compounds across each asset.

The Lookback Option (and Its Limits)

Property owners who've held a building for years without a cost segregation study aren't out of options. IRS Form 3115 allows a change in accounting method that captures all missed depreciation in a single year — no amended returns required. Seneca handles Form 3115 preparation as part of lookback studies.

The lookback approach works best when timed strategically:

- High current-year income: Maximizes the value of the catch-up deduction, since you have more taxable income to offset

- At or near acquisition: Avoids Form 3115 complexity entirely and captures the full time-value of early deductions

Timing Relative to the Tax Year

Studies completed before your return is filed apply cleanly to the current year. Studies completed after filing require Form 3115 adjustments. Both are workable, but early action simplifies the process and preserves maximum flexibility.

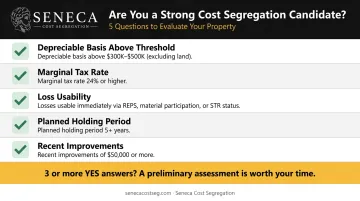

How to Evaluate Your Property's ROI Potential

Before committing to a study, run through this five-question checklist:

- Is my depreciable basis above $300,000–$500,000 (excluding land)?

- Is my marginal tax rate 24% or higher?

- Can I use the losses immediately — do I qualify for REPS, material participation, or STR non-passive treatment?

- Is my planned holding period 5+ years?

- Have I made significant recent improvements ($50,000+) that created fresh depreciable basis?

If you answer yes to three or more of these, a preliminary assessment is worth your time.

Seneca Cost Segregation offers complimentary estimates before any engagement. Each estimate includes projected reclassification amounts, estimated first-year savings, and the expected return multiple for your specific property. Studies are completed within 2–4 weeks and backed by the AuditDefense guarantee: if an audit reveals their study caused a depreciation adjustment exceeding 5%, they refund 100% of study fees.

Your CPA should be part of this evaluation. Cost segregation interacts with entity structure, income type, and overall tax strategy — the study should be reviewed in context of your full tax picture, not in isolation.

Frequently Asked Questions

Is it worth doing a cost segregation study?

For properties with a depreciable basis above $500,000 and an owner in the 24%+ tax bracket, cost segregation studies consistently generate returns of 10–40x the study fee in year one. Few tax strategies deliver that kind of return on a fixed-fee engagement.

What is the minimum property value for cost segregation to make financial sense?

Most specialists recommend a depreciable basis of at least $300,000–$500,000 (excluding land). Below that threshold, study fees can eat into savings — though properties with significant improvements may still qualify below the floor.

How long does it take for a cost segregation study to pay for itself?

For qualifying properties, payback is typically achieved within weeks of filing — first-year tax savings routinely exceed study costs by a wide margin. Payback measured in years is the exception, not the norm.

Can I do a cost segregation study on a property I've already owned for several years?

Yes. IRS Form 3115 allows property owners to recover missed depreciation from prior years in a single catch-up deduction — no amended returns required. Studies completed at acquisition capture the most value, but lookback studies can still generate substantial savings years later.

What happens to accelerated depreciation when I sell the property?

Depreciation recapture applies at a 25% rate on unrecaptured Section 1250 gain at sale. Over a 5+ year hold, the time-value of first-year savings typically exceeds recapture costs. A 1031 exchange defers recapture indefinitely.

Does my tax bracket significantly affect cost segregation ROI?

Directly. Investors in the 37% bracket save $37,000 per $100,000 of reclassified assets versus $24,000 at the 24% bracket. Along with property basis and hold period, tax bracket is one of the three primary inputs in any ROI projection — the difference between brackets can swing net savings by five figures on a single study.