This article explains how short-term rentals (STRs) are taxed, the key qualifications that unlock favorable treatment, and how cost segregation and bonus depreciation create large first-year deductions that reduce taxable income by tens - or even hundreds - of thousands of dollars. We'll also cover what you need to do to stay compliant and defend your position if the IRS comes calling.

TLDR: Key Takeaways

- Rentals averaging 7-day or shorter guest stays can bypass passive loss rules (IRC §469), letting losses offset W-2 income.

- Owners must still prove material participation by satisfying at least one of the IRS's seven tests.

- Cost segregation and 100% bonus depreciation (restored in 2025) generate large deductions that create offsetting losses.

- Detailed records of hours worked and guest stays are essential to survive an IRS audit.

How the IRS Taxes Short-Term Rental Income

Under IRC Section 469, rental activities are automatically classified as passive, even if you work full-time managing the property. Losses from your vacation rental can only offset other passive income - not your W-2 wages or business income.

If you generate a $50,000 paper loss through depreciation but have no passive gains to absorb it, that loss is suspended and unusable until you sell the property or earn passive income from another source.

This passive classification is the default for all rental real estate. The IRS doesn't care how much time you spend managing bookings or responding to guest requests - under the standard rule, it's still passive.

Passive vs. Non-Passive: Why the Distinction Matters

Non-passive (active) rental activity changes everything. Losses from non-passive activities can offset any income type - W-2 wages, self-employment income, including portfolio income like dividends. For high-income earners, this makes the tax benefit immediate and powerful.

One path to non-passive treatment is Real Estate Professional Status (REPS). To qualify, you must meet two thresholds:

- More than 750 hours per year spent in real estate trades or businesses

- More than half of your total working hours devoted to real estate

For most full-time employees, REPS is out of reach. That's where the STR loophole becomes relevant - but it operates under an entirely different set of rules than the 14-day rule below.

The 14-Day Rule: A Simpler Tax Break for Occasional Renters

If you rent your property for 14 days or fewer per year and personally use it for more than 14 days, a specific IRS rule applies:

- Rental income is not reported - you pocket it tax-free

- Rental expense deductions are not allowed for that property

- This rule applies to occasional renters only, not active STR operators

This is a completely separate provision from the STR loophole. Knowing which rule applies to your situation determines which deductions - if any - are available to you.

The STR Tax Loophole: How to Qualify

The STR loophole is a legal tax strategy rooted in IRS exceptions under IRC Section 469. When you meet specific conditions, your vacation rental is reclassified from a passive rental into a non-passive business activity, enabling losses to offset ordinary income without qualifying for REPS.

Two conditions must both be satisfied simultaneously:

- The property must meet the average rental period test

- The owner must materially participate

The 7-Day Average Stay Rule

The core qualifying criterion: the average period of customer use must be 7 days or fewer across all rentals during the tax year. Calculate this by dividing total rental days by the number of rental periods - not by setting individual stay limits.

Example:

- 10 bookings totaling 60 rental days = 60 ÷ 10 = 6-day average (qualifies)

- 8 bookings totaling 70 rental days = 70 ÷ 8 = 8.75-day average (does not qualify)

The IRS does recognize alternative paths - an average stay of 30 days or less with significant personal services, or extraordinary personal services regardless of stay length - but for most Airbnb and VRBO owners, the 7-day rule is the clearest route.

Material Participation Tests

Clearing the 7-day threshold gets you out of the "rental activity" classification - but that alone doesn't unlock the tax offset. To achieve non-passive status and apply losses against ordinary income, you must also prove material participation under one of seven IRS tests.

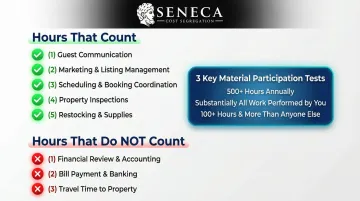

The three most practical tests for STR investors:

- 500+ hours spent on the STR activity during the year

- Substantially all the work is performed by the owner

- 100+ hours, and more than any other individual (including cleaners, managers, contractors)

Watch out if you use a property manager. Hiring one can quietly undermine the third test. If your manager logs 120 hours and you log only 110, you fail - even if you were deeply involved. Either exceed the manager's hours or qualify under a different test, such as the 500-hour threshold.

Hours that count toward participation:

- Guest communication and booking coordination

- Marketing and listing management

- Scheduling cleaners and contractors

- Property inspections and repairs coordination

- Supply restocking and staging

Hours that do not count:

- Reviewing financial statements (investor activity)

- Paying bills or transferring funds

- Travel time to and from the property

Log your hours in real time. Keep a contemporaneous activity log with dates, tasks, and duration - the Tax Court routinely rejects "postevent ballpark guesstimates" and demands verifiable records. Overstating hours is one of the most common audit triggers for STR investors.

Cost Segregation and Bonus Depreciation: The Engine Behind Big STR Tax Savings

Even after qualifying as non-passive, the tax benefit is limited without a mechanism to generate large deductions. Depreciation is that mechanism - but the standard 39-year depreciation schedule for commercial property is too slow to create meaningful first-year losses.

A cost segregation study solves this problem. This engineering-based analysis reclassifies portions of a property's purchase price into shorter depreciation categories:

- 5-year property: Appliances, carpet, fixtures

- 7-year property: Equipment, furnishings

- 15-year property: Landscaping, parking, fencing

Rather than depreciating the entire building over 39 years, a cost segregation study typically reclassifies 20–40% of the property's depreciable basis into these accelerated categories.

Illustrative Example:

You purchase a vacation rental for $600,000 (land = $100,000, building = $500,000).

- Without cost segregation: $500,000 ÷ 39 years = $12,821 annual depreciation

- With cost segregation: 30% reclassified into 5-, 7-, and 15-year property = $150,000 eligible for bonus depreciation in year one

100% Bonus Depreciation Restored

Under the "One, Big, Beautiful Bill Act" (Public Law 119-21), enacted July 4, 2025, 100% bonus depreciation has been permanently restored for qualifying property acquired on or after January 20, 2025. This means you can deduct 100% of the cost of qualifying short-life assets in the year they are placed in service, rather than spreading those deductions across 5, 7, or 15 years.

When a qualifying STR generates non-passive losses through cost segregation and bonus depreciation, a high-income W-2 earner can potentially reduce taxable income by tens or hundreds of thousands of dollars in year one.

Getting the Numbers Right: Why Study Quality Matters

Those deductions only hold up if the underlying study is IRS-compliant. A poorly documented reclassification can be reversed on audit - wiping out the savings entirely. That's where a qualified engineering firm makes the difference.

Seneca Cost Segregation has completed over 10,200 engineering-based studies across all 50 states, averaging $171,243 in first-year deductions per property. Key differentiators include:

- Study turnaround: Completed within 2–4 weeks

- Methodology: Building-to-blueprint engineering analysis, not desktop estimates

- Audit protection: AuditDefense included with every study

- Track record: 95% client referral rate over 12+ years in business

For STR owners targeting first-year losses, the study documentation is as important as the strategy itself.

Additional Tax Deductions for Your Vacation Rental

Beyond depreciation, STR owners can deduct a range of ongoing expenses:

- Mortgage interest (prorated if personal use applies)

- Property taxes

- Insurance premiums

- Utilities

- Repairs and maintenance

- Cleaning and turnover costs

- Platform fees (Airbnb, VRBO)

- Supplies provided to guests

- Advertising costs

Several of these deductions come with conditions worth knowing before you file.

Personal Use Allocation Rule

If you personally use the property for more than 14 days or 10% of rental days (whichever is greater), expenses must be prorated between personal and rental use. Only the rental-use portion is deductible.

Self-Employment Tax Consideration

If you provide substantial hospitality-style services, such as daily cleaning, meals, or concierge assistance, the IRS may treat your rental as an active business rather than a passive investment. That classification triggers self-employment tax on top of ordinary income tax. A qualified tax advisor can assess whether your service level crosses that threshold and help you structure accordingly.

Compliance, Documentation, and Audit Risks

Used correctly, the STR loophole is fully legal - but it draws consistent IRS scrutiny. The combination of non-passive losses offsetting W-2 income and large depreciation deductions is a recognized audit trigger. Prepare documentation before filing, not after an audit notice.

Documentation Checklist

- Contemporaneous log of hours spent on the rental (date, activity, duration)

- Guest reservation records confirming average stay calculation

- Receipts and invoices for all deductible expenses

- Cost segregation study report prepared by a qualified engineering firm

- Contractor/cleaner hours logs to demonstrate material participation superiority

Common Mistakes That Invalidate the Loophole

- Manipulating lease language rather than tracking actual average stay

- Failing to track hours until year-end

- Excessive personal use days reducing the rental portion

- Not having a formal cost segregation study to support accelerated depreciation claims

The IRS Passive Activity Loss Audit Technique Guide specifically identifies STRs as audit targets. Examiners verify average rental periods and demand proof of material participation - and without thorough documentation, your entire tax position is at risk.

Frequently Asked Questions

Can I use short-term rental losses to offset my W-2 income?

Yes, if the property qualifies under the 7-day average stay rule and you materially participate. Losses are treated as non-passive and can offset W-2 wages, but both conditions must be met simultaneously.

What is the 7-day rule for short-term rentals?

The 7-day rule means the average rental period across all guest stays during the year must be 7 days or fewer, calculated by dividing total rental days by the number of rental transactions.

Can I hire a property manager and still qualify for the STR loophole?

Using a property manager is allowed, but it complicates material participation. If the manager logs more hours than you, you lose qualification under the "more than anyone else" test. You must then satisfy one of the remaining tests, such as the 500-hour threshold.

How much can a cost segregation study save me on a vacation rental?

Savings vary based on purchase price, property type, and applicable bonus depreciation. Seneca Cost Segregation's average client achieves first-year tax savings of $171,243 - though your result depends on your specific property. Request a free assessment for a precise estimate.

What records do I need to prove material participation to the IRS?

Maintain a real-time activity log with dates and hours, evidence of guest communication and management activities, and records showing other participants such as contractors spent fewer hours than you.

How is a short-term rental taxed differently than a long-term rental?

Long-term rentals are almost always passive, while short-term rentals can qualify as non-passive with the right structure. STRs use a 39-year depreciation schedule rather than 27.5 years, but cost segregation can accelerate deductions more aggressively in the short term.