Cost segregation is the engineering-based process that separates those components and front-loads your depreciation deductions. For QSR owners, the financial impact can be immediate and substantial — often six figures in year one.

This article is for QSR and fast food property owners, franchisees who own their buildings, and real estate investors holding restaurant properties. We'll walk through a representative case study showing how a typical fast food acquisition gets analyzed, what the asset breakdown looks like, and what the tax savings actually amount to.

Key Takeaways

- Cost segregation reclassifies fast food restaurant components into 5-, 15-, and 39-year categories, front-loading deductions that normally stretch over decades

- Fast food properties qualify at unusually high rates due to drive-thru infrastructure, specialized kitchen systems, and large paved site footprints

- First-year tax savings on a typical $1M–$2M QSR acquisition commonly range from $100,000 to $350,000+

- Prior-year purchases still qualify — missed deductions can be claimed today via Form 3115 without amending past returns

- An engineering-based study is required for IRS defensibility — software estimates leave money on the table and carry higher audit risk

Why Fast Food Restaurants Are Prime Candidates for Cost Segregation

Standard commercial real estate depreciates over 39 years using straight-line MACRS. The IRS treats the building as one asset — but a fast food restaurant is anything but a generic building.

A Unique Asset Profile

Fast food properties contain a high concentration of components with shorter functional lifespans:

- Commercial kitchen systems — fryers, grills, exhaust hoods, grease traps, make-up air units, and the electrical/plumbing dedicated to them

- Drive-thru infrastructure — speaker and ordering systems, dedicated lane paving, canopies, and menu board structures

- POS systems and dedicated wiring — registers, kiosks, and their equipment-specific electrical circuits

- Interior finishes and millwork — counters, booth seating, decorative lighting, and floor coverings that are readily removable

- Signage systems — exterior illuminated signs and their electrical feeds

The IRS specifically classifies restaurant equipment as 5-year property — compared to the 7-year treatment most other business equipment receives. That means QSR owners can front-load depreciation deductions in the earliest years of ownership, improving after-tax cash flow when it matters most.

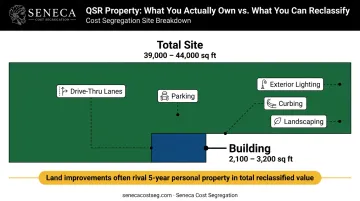

The Site Footprint Advantage

The ratio of land improvements to building size makes fast food properties especially strong candidates. A typical QSR building runs 2,100–3,200 square feet, but the total site often spans 39,000–44,000 square feet. That surrounding acreage — drive-thru lanes, parking, exterior lighting, curbing, and landscaping — qualifies as 15-year land improvements, not 39-year building components. In many QSR studies, this category rivals or exceeds the 5-year personal property bucket in total value.

Qualifying Events and Retroactive Opportunities

Cost segregation studies are triggered by:

- Property acquisition (purchase or construction)

- Significant renovation or remodel

- Long-held properties where no prior study was completed

Owners who purchased years ago and never ran a study can still capture all missed depreciation. The IRS allows a lookback study using Form 3115, which lets you claim the accumulated catch-up deduction in a single current tax year — no amended returns required.

Fast Food Restaurant Cost Segregation: Case Study Overview

To show how this plays out in practice, consider a representative QSR acquisition with the following profile:

| Property Detail | Value |

|---|---|

| Purchase Price (excluding land) | $1,500,000 |

| Building Square Footage | ~2,800 sq ft |

| Total Site Square Footage | ~42,000 sq ft |

| Combined Tax Rate Assumed | 35% |

| Bonus Depreciation Applied | Yes (40% — current 2025 rate) |

This scenario is consistent with real-world benchmarks from published QSR cost segregation studies — KBKG's fast food case study documented $356,158 in first-year savings on a $1.06M property, while CSSI's comparable study showed $243,296 in savings on a $1.335M acquisition. This scenario is consistent with real-world benchmarks from published QSR cost segregation studies — KBKG's fast food case study documented $356,158 in first-year savings on a $1.06M property, while CSSI's comparable study showed $243,296 in savings on a $1.335M acquisition. The methodology behind those results is what separates defensible studies from ones that leave money on the table.

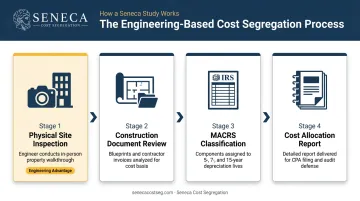

How an Engineering-Based Study Works

A credible study involves four core components:

- Physical site inspection — Engineers walk the property and document every component, photographing systems and measuring fixtures

- Construction document review — Blueprints, contractor invoices, and closing statements are analyzed to confirm cost allocations

- MACRS classification — Each identified component is assigned its correct depreciation life per IRS guidelines

- Detailed cost allocation report — The final deliverable reconciles every dollar of depreciable basis to its appropriate asset class

Software-only tools skip Step 1. On a $1.5M property, that shortcut can leave $30,000–$50,000 in legitimate deductions unclaimed.

It also creates a weaker paper trail. The IRS Cost Segregation Audit Techniques Guide explicitly recognizes engineering-based studies as more reliable — a distinction that matters if your return gets scrutinized.

What Engineers Physically Evaluate

QSR properties have an unusually high concentration of short-life assets — drive-thru infrastructure, specialized electrical systems, and food-service plumbing that standard depreciation schedules miss entirely. The site inspection captures all of it:

- Kitchen layout, equipment connections, and hood/ventilation systems

- Drive-thru lane paving, canopy structures, and ordering equipment

- Interior finishes, counters, millwork, and removable flooring

- Specialized electrical panels serving signage, cooking equipment, and POS systems

- Plumbing configurations for food service and grease management

- Exterior improvements: asphalt, concrete curbing, site lighting, and landscaping

Asset Classification Results: Where the Tax Savings Hide

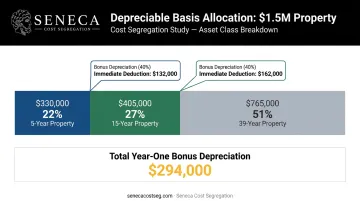

5-Year Property (~22% of Depreciable Basis)

On our $1.5M property, approximately $330,000 falls into this category.

Qualifying components include:

- Commercial kitchen equipment and dedicated electrical/plumbing connections

- POS systems and their circuits

- Interior decorative finishes, counters, and millwork

- Removable floor coverings

- Specialized exhaust and ventilation systems

15-Year Property (~27% of Depreciable Basis)

Approximately $405,000 lands here — typically the second-largest category, and sometimes the largest in drive-thru-heavy properties.

This covers all land improvements:

- Drive-thru lane and parking lot paving (asphalt and concrete)

- Exterior lighting and poles

- Landscaping and irrigation

- Signage bases and monument sign foundations

- Utility connections and site drainage

39-Year Property (~51% of Depreciable Basis)

Roughly $765,000 remains on the standard schedule — the structural shell, load-bearing walls, roof structure, standard wiring, and core plumbing. Without a study, all $1.5M would sit here.

The table below shows how the full $1.5M depreciable basis breaks down across all three classes.

Asset Allocation Summary

| Asset Class | Dollar Amount | % of Depreciable Basis |

|---|---|---|

| 5-Year Property | $330,000 | 22% |

| 15-Year Property | $405,000 | 27% |

| 39-Year Property | $765,000 | 51% |

| Total | $1,500,000 | 100% |

How Bonus Depreciation Amplifies the Result

The 5-year and 15-year reclassified assets qualify for bonus depreciation, currently 40% in 2025. That rate has been phasing down from 100% under current law, though the One Big Beautiful Bill Act is moving through Congress and may restore higher rates. Here's how the math plays out for this property:

- $330,000 × 40% bonus = $132,000 immediate deduction (5-year assets)

- $405,000 × 40% bonus = $162,000 immediate deduction (15-year assets)

That's $294,000 in bonus depreciation alone, on top of the first-year MACRS deductions on the remaining basis.

The Financial Outcome: Real Tax Savings in Action

First-Year Tax Savings

Using a 35% combined tax rate, the accelerated deductions from our representative study generate a first-year tax savings of approximately $120,000–$150,000 from bonus depreciation alone. Adding in the regular MACRS deductions on the reclassified basis pushes total first-year savings well above what straight-line depreciation would have produced.

Across Seneca's completed restaurant studies, properties with higher purchase prices or higher bonus depreciation rates regularly produce first-year savings exceeding $250,000.

Net Present Value Over 10 Years

Even though deductions are front-loaded, the long-term NPV advantage is significant. Using an 8% present value assumption, the NPV of accelerated depreciation savings over a 10-year hold typically falls in the $100,000–$205,000 range compared to straight-line depreciation — reflecting the time value of money on deductions taken now rather than spread over four decades.

What That Capital Can Fund

For a fast food operator, six-figure first-year savings translate directly into reinvestment capacity. That cash can:

- Fund equipment upgrades (new fryers, beverage dispensers, drive-thru ordering technology)

- Cover rising labor costs without touching operating reserves

- Serve as seed capital toward a second franchise location

ROI of the Study

A professional engineering-based cost segregation study on a restaurant property in the $1M–$2M range typically costs $7,000–$15,000, depending on complexity and documentation availability. Against first-year savings of $100,000–$250,000, the ROI is often 10x–20x the study fee in year one alone — and that figure grows further when the NPV of deductions across the full holding period is included. Seneca offers a complimentary savings estimate before any commitment, so operators can verify projected returns for their specific property before engaging.

What to Do Next: Starting a Cost Segregation Study for Your Restaurant

Do You Qualify?

Check these basics:

- Property is income-producing or business-use real estate

- Purchase price (excluding land) is $200,000 or more

- Property was placed in service after 1986

- You own the building — not just the franchise rights

Both newly acquired properties and those purchased years ago qualify. A lookback study on a property held for five or ten years can generate a substantial catch-up deduction in the current tax year.

What the Process Looks Like

The process has four steps:

- Complimentary assessment — Share basic property details (purchase price, square footage, acquisition date) and receive a preliminary savings estimate

- Intake and documentation — Provide closing statements, depreciation schedules, and any available construction documents

- Site inspection and analysis — Engineers conduct a physical or virtual inspection and classify every component

- Study delivery — A complete engineering report, depreciation schedules, and Form 3115 preparation (if needed for a lookback study) are delivered within 2–4 weeks

Seneca Cost Segregation completes studies nationwide within this timeframe, and CPA coordination support is included at no additional charge so your tax professional can implement the findings directly.

Choosing the Right Provider

Not all cost segregation providers follow the same standards — and the IRS notices the difference. The American Society of Cost Segregation Professionals requires engineering methodology as the foundation of any defensible study.

Seneca's team holds CCSP certification through the ASCSP and has completed over 10,200 studies across all 50 states. Every study includes an AuditDefense guarantee: if an audit reveals that Seneca's study caused a depreciation adjustment exceeding 5%, they refund 100% of study fees. No Seneca client has faced an adverse audit outcome to date.

Frequently Asked Questions

What building components of a fast food restaurant qualify for accelerated depreciation?

Depreciation life breaks down across three buckets:

- 5-year: Kitchen equipment connections, specialized electrical for cooking and POS systems, interior millwork, and removable finishes

- 15-year: Drive-thru paving, parking lots, exterior lighting, and landscaping

- 39-year: The structural shell — walls, roof, and core systems

How much can a fast food restaurant owner realistically save with a cost segregation study?

Savings depend on property value, tax rate, and the applicable bonus depreciation rate. On a typical QSR acquisition in the $1M–$2M range, first-year savings commonly fall between $100,000 and $350,000+. Properties with larger site footprints or higher bonus depreciation rates trend toward the top of that range.

Can I do a cost segregation study on a fast food restaurant I purchased several years ago?

Yes. The IRS allows lookback studies on properties placed in service since 1986. All accumulated missed deductions are claimed as a single catch-up adjustment in the current tax year via Form 3115 — no amended returns required.

Does cost segregation work for fast food franchisees, or only building owners?

Cost segregation applies only to property owners. Franchisees who lease their location cannot use it. However, franchisees who own the building — or the underlying real estate — qualify fully and often see high reclassification percentages due to the specialized fit-out of QSR properties.

How long does a cost segregation study take for a restaurant property?

A qualified engineering-based firm typically delivers a completed study within 2–4 weeks of receiving property documentation and completing the site inspection. Virtual inspections often allow for delivery in the shorter end of that range.

Will conducting a cost segregation study increase my chances of an IRS audit?

A properly conducted engineering-based study does not increase audit risk. The IRS has published a Cost Segregation Audit Techniques Guide that explicitly acknowledges the practice as legitimate. A credentialed provider will deliver a defensible report and provide audit support if the IRS ever inquires.