This guide covers the MACRS property classes that apply to restaurant assets, how to build a depreciation schedule, 2025 acceleration rules, and how cost segregation can squeeze significantly more value out of a restaurant build-out.

Key Takeaways

- Most restaurant equipment (ovens, refrigerators, POS systems, booths) qualifies as 5-year MACRS property under Asset Class 57.0

- The 2025 Section 179 limit is $2,500,000; property acquired after January 19, 2025 qualifies for 100% bonus depreciation

- Qualified improvement property (QIP) recovers over 15 years—not 39—and qualifies for bonus depreciation

- A cost segregation study can reclassify 23–40% of a restaurant build-out to shorter depreciation lives—accelerating deductions that can generate five- to six-figure first-year tax savings

- Common mistake to avoid: Misclassifying equipment as 39-year building property is the single costliest depreciation error restaurant owners make

What Is MACRS Depreciation and How Does It Apply to Restaurant Equipment?

IRS Publication 946 establishes MACRS (Modified Accelerated Cost Recovery System) as the required depreciation method for most business property placed in service after 1986. Under MACRS, the IRS assigns each asset to a specific property class with a fixed recovery period and depreciation method—restaurant owners cannot choose their own schedule.

GDS vs. ADS: Two Systems, Different Outcomes

MACRS operates through two systems:

- General Depreciation System (GDS): Uses accelerated declining-balance methods for personal property, front-loading deductions into early years. This is the default and most advantageous for most restaurant owners.

- Alternative Depreciation System (ADS): Uses straight-line depreciation over longer periods. Required for specific situations—property used predominantly outside the U.S., tax-exempt use property, listed property used 50% or less for business, and property of an electing real property trade or business under Section 163(j). Electing ADS forfeits bonus depreciation eligibility.

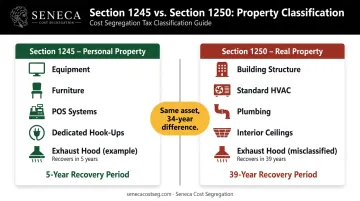

Section 1245 vs. Section 1250: The Classification That Drives Everything

This distinction determines how fast an asset depreciates:

- Section 1245 property (personal property): Equipment, furniture, POS systems, dedicated equipment hook-ups. Recovery period is typically 5 or 7 years under MACRS.

- Section 1250 property (real property): Building structure, standard plumbing, general HVAC, interior ceilings — 39-year recovery life. Standard building components land here regardless of their function in your restaurant.

Getting this classification right is worth real money. A commercial exhaust hood properly classified as Section 1245 property recovers its cost in 5 years. Misclassified as Section 1250 building property, that same hood depreciates over 39 years.

One important side note: when you eventually sell equipment classified as Section 1245 property, gains up to the amount of depreciation claimed are recaptured as ordinary income — not capital gains. That recapture risk is manageable, but worth knowing before you classify aggressively.

The table below shows how common restaurant assets map to these classifications and their corresponding MACRS recovery periods.

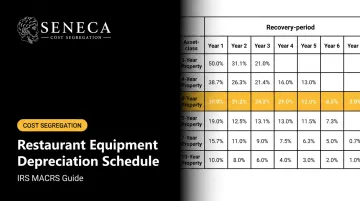

Restaurant Equipment MACRS Property Classes and Recovery Periods

The IRS Cost Segregation Audit Technique Guide (Pub. 5653) specifically addresses restaurants under Asset Class 57.0 – Distributive Trades and Services, with a 5-year GDS recovery period. Knowing which assets fall under each class determines how fast you recover costs — and where a cost segregation study can accelerate that timeline.

MACRS Reference Table for Restaurant Assets

| Asset Category | MACRS Class | GDS Recovery Period |

|---|---|---|

| Cooking equipment (ovens, fryers, ranges) | 57.0 | 5 years |

| Refrigeration and beverage equipment | 57.0 | 5 years |

| Food prep and storage equipment | 57.0 | 5 years |

| Restaurant furniture and booth seating | 57.0 | 5 years |

| Bar stools, non-structural décor | 57.0 | 5 years |

| POS systems and computers | 57.0 | 5 years |

| Decorative millwork, crown molding | 57.0 | 5 years |

| Dedicated equipment hook-ups (gas lines to fryers, water lines to steam trays) | 57.0 | 5 years |

| Office furniture and fixtures | General | 7 years |

| Qualified improvement property (QIP) | QIP | 15 years |

| General HVAC and plumbing serving the building | Nonresidential real | 39 years |

| Restaurant building structure | Nonresidential real | 39 years |

| Interior ceilings | Nonresidential real | 39 years |

The "Placed in Service" Rule and Conventions

Depreciation starts when equipment is ready and available for use—not when you pay the invoice or take delivery. A walk-in cooler installed in December but not yet operational does not start depreciating until it's ready to run.

Two conventions affect first-year deductions:

- Half-year convention: Default for most restaurant equipment. Treats all property as placed in service at midyear, giving you a half-year of depreciation regardless of actual purchase date.

- Mid-quarter convention: Triggered when more than 40% of your total depreciable basis is placed in service in Q4. Under this convention, Q4 assets only receive 1.5 months of depreciation instead of 6, which can meaningfully reduce your first-year deduction if you're making large equipment purchases late in the year.

How 5-Year GDS Depreciation Works: A Practical Example

Understanding those conventions in practice matters most when you're projecting actual deductions. Under GDS, 5-year property uses the 200% declining balance method, which front-loads deductions then switches to straight-line when that becomes more beneficial.

Using IRS Publication 946, Table A-1 percentages, here's what a $50,000 commercial oven looks like over its recovery period (half-year convention):

| Year | IRS % | Annual Deduction | Accumulated Depreciation |

|---|---|---|---|

| 1 | 20.00% | $10,000 | $10,000 |

| 2 | 32.00% | $16,000 | $26,000 |

| 3 | 19.20% | $9,600 | $35,600 |

| 4 | 11.52% | $5,760 | $41,360 |

| 5 | 11.52% | $5,760 | $47,120 |

| 6 | 5.76% | $2,880 | $50,000 |

Note that cost recovery spans 6 tax years despite being "5-year property"—the half-year convention splits the first and last years.

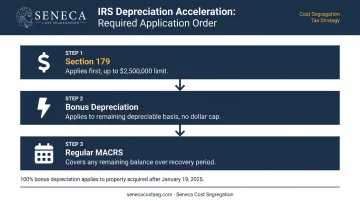

Section 179 and Bonus Depreciation for Restaurant Equipment in 2025

These two tools let qualifying restaurants compress years of depreciation into a single tax year.

Section 179 Expensing

Restaurant owners can elect to deduct the full cost of qualifying equipment in the year it's placed in service rather than depreciating it over the recovery period.

2025 limits (per IRS Publication 946):

- Maximum deduction: $2,500,000

- Phase-out begins at: $4,000,000 in qualifying property placed in service

- Full phase-out at: $6,500,000 (zero Section 179 deduction)

- Cannot exceed taxable income from active business operations; excess carries forward

Section 179 applies to 5-year and 7-year restaurant equipment and qualified real property categories including QIP.

Bonus Depreciation in 2025: A Major Change

The One Big Beautiful Bill Act (P.L. 119-21) reinstated 100% bonus depreciation, reversing the phase-down schedule that had been in effect.

| Property Acquisition Date | Bonus Depreciation Rate |

|---|---|

| Acquired after January 19, 2025 | 100% |

| Acquired before January 20, 2025, placed in service in 2025 | 40% |

Unlike Section 179, bonus depreciation has no dollar cap and can generate a net operating loss—making it useful for restaurants with large equipment purchases that exceed taxable income.

Combining the Two Strategies

Per IRS rules, the application order is:

- Section 179 applies first, up to its dollar limit

- Bonus depreciation applies to the remaining depreciable basis

- Regular MACRS covers whatever's left

A restaurant that purchases $300,000 of qualifying kitchen equipment in 2025 can expense the full amount in year one through Section 179 or bonus depreciation, subject to income limitations.

What Doesn't Qualify

Not everything in a restaurant qualifies for acceleration:

- Land and land improvements classified as 39-year property

- Structural building components (ceilings, exterior walls, general HVAC)

- Property used predominantly outside the U.S.

- Inventory

- Property required to use ADS (ineligible for bonus depreciation)

Recapture risk: If Section 179 or bonus depreciation is claimed and business use drops below 50% before the recovery period ends, the IRS requires recapture of excess depreciation as ordinary income.

How to Build a Restaurant Equipment Depreciation Schedule

Determining Your Cost Basis

The depreciable basis of restaurant equipment includes more than the purchase price. Add to the asset's cost basis — rather than expense immediately — all costs required to make it ready for service:

- Purchase price and applicable sales tax

- Freight and delivery charges

- Installation and mounting costs

- Testing, calibration, and commissioning fees

Group assets purchased and disposed of together as a single line item to simplify tracking.

The Fixed Asset Register

A proper depreciation schedule documents each asset with:

- Description and serial number

- Placed-in-service date

- Cost basis

- MACRS property class and recovery period

- Convention (HY or MQ)

- Depreciation method

- Annual depreciation amount

- Accumulated depreciation

- Remaining book value

Form 4562 (Depreciation and Amortization) must be filed with your tax return to claim these deductions. The 2025 version adds lines 19h and 20e for 50-year property.

Repair vs. Capitalization

Whether a cost is a repair or a capital improvement determines whether you deduct it this year or depreciate it over time:

- Repair (fully deductible now): Routine maintenance keeping equipment operational—replacing a broken seal, lubricating moving parts, cleaning a condenser coil

- Capitalize and depreciate: Improvements that extend useful life, adapt equipment to new uses, or restore it to like-new condition

Treasury Reg. §1.263(a)-3 governs this distinction. When a compressor replacement on a walk-in cooler costs $8,000, the question isn't the dollar amount—it's whether the work constitutes a betterment, restoration, or adaptation under the regulation. In most cases, replacing a major component like a compressor qualifies as a restoration and must be capitalized, not expensed.

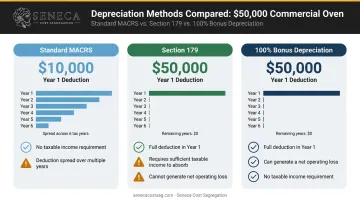

Practical Example: A 5-Year Depreciation Schedule

Commercial oven purchased for $50,000, placed in service Year 1:

| Election | Year 1 Deduction | Years 2–7 Deduction |

|---|---|---|

| Standard MACRS (no acceleration) | $10,000 | Per IRS Table A-1 |

| Section 179 only | $50,000 | $0 |

| 100% Bonus depreciation only | $50,000 | $0 |

Standard MACRS spreads the deduction across 6 tax years (years 1–6 under the half-year convention). Section 179 and bonus depreciation both collapse the full $50,000 into year one, but with a key difference: Section 179 requires sufficient taxable income to absorb the deduction, while bonus depreciation can generate a net operating loss that carries forward to future years.

Both acceleration options apply to equipment acquired after January 19, 2025.

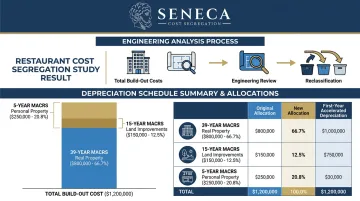

How Cost Segregation Can Accelerate Restaurant Depreciation

Most restaurant owners who own their building—or completed a significant tenant build-out—are sitting on depreciation they haven't claimed.

What a Cost Segregation Study Does

A cost segregation study is an engineering-based tax analysis that separates a restaurant's construction costs into the correct MACRS classes rather than defaulting everything to 39 years. Components that the IRS Cost Segregation ATG specifically identifies as reclassifiable in restaurants include:

- 5-year property: Beverage equipment and dispensing systems, kitchen equipment hook-ups (dedicated gas lines, separate water lines to steam trays), booth seating, bar stools, decorative millwork

- 15-year property: Qualified improvement property—interior renovations, flooring upgrades, specialty plumbing infrastructure

Standard building plumbing, interior ceilings, and the base building shell remain 39-year property. The engineering analysis separates the two categories with documentation that supports the classification under IRS scrutiny.

The Tax Impact

Restaurants achieve some of the highest reclassification rates among commercial property types—23–40% of total build-out costs move to shorter depreciation schedules. That means a restaurant owner who spent $800,000 on a build-out might find $185,000–$320,000 eligible for 5-year or 15-year treatment instead of 39-year recovery.

Seneca Cost Segregation's engineering-based studies have produced an average first-year deduction of $171,243 across more than 10,200 completed studies nationwide. For restaurant properties specifically, which contain dense concentrations of specialized equipment and fixtures, results fall at the higher end of the reclassification range.

Look-Back Studies for Existing Restaurant Properties

Restaurant owners who have never commissioned a cost segregation study don't have to amend prior returns. A look-back study calculates the difference between depreciation actually claimed and what cost segregation would have produced, then captures that entire difference as a Section 481(a) catch-up adjustment in the current year—filed via Form 3115 alongside the current return.

This approach works for properties as far back as January 1, 1987, though properties older than 10 years rarely justify the study cost. For a restaurant acquired or renovated within the last decade, a look-back study often recovers five or more years of missed deductions in a single filing.

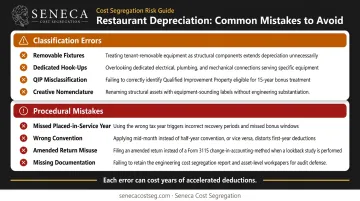

Common Depreciation Mistakes Restaurant Owners Must Avoid

Classification Errors That Cost the Most

- Treating removable fixtures as 39-year property: Booth seating, portable partitions, and non-structural décor are 5-year personal property under ATG examples—not building components.

- Failing to separate dedicated equipment hook-ups: Dedicated gas lines to fryers and separate water lines to steam trays are 5-year Section 1245 property. Standard building plumbing serving the structure is 39-year property. Lumping them together costs years of accelerated deductions.

- Treating all QIP as 39-year property: Interior improvements to nonresidential buildings placed in service after the building's original placed-in-service date recover over 15 years, not 39, and qualify for bonus depreciation.

- Creative nomenclature: The IRS ATG explicitly warns against renaming water piping as "process piping" or an emergency exit sign as a "decorative placard" to justify shorter lives. Documentation must match engineering reality.

Classification errors determine the starting point — but procedural mistakes at filing can undo even a correctly classified asset. The errors below are where real money gets left on the table.

Procedural Mistakes

- Missing the placed-in-service year: You cannot retroactively claim a year's depreciation without filing Form 3115 or amending the return. Skipping year one is a real cost.

- Wrong convention: Applying the half-year convention when the mid-quarter convention is required reduces first-year deductions for Q4 equipment purchases.

- Using amended returns for established methods: If you've applied an impermissible depreciation method for two or more consecutive years, Form 3115 is required—not an amended return.

- Missing documentation: Purchase invoices, installation records, and placed-in-service dates are the backbone of any audit defense. Without them, the IRS can disallow deductions regardless of correct classification.

Frequently Asked Questions

What is the depreciation schedule for restaurant equipment?

Most restaurant equipment—ovens, refrigerators, fryers, POS systems, furniture—falls under MACRS 5-year property using Asset Class 57.0. The cost recovers over 5 tax years (6 calendar years under the half-year convention) using the 200% declining balance method, though Section 179 or bonus depreciation can compress the entire deduction into year one.

What is MACRS depreciation for equipment?

MACRS is the IRS-required depreciation system for business property placed in service after 1986. It assigns each asset to a property class with a specific recovery period and method—usually accelerated declining balance for personal property. This front-loads deductions into early years, when equipment delivers the most value to the business.

Can I deduct restaurant equipment in the first year I buy it?

Yes. Section 179 allows full first-year expensing up to the $2,500,000 annual limit, and 100% bonus depreciation applies to qualifying property acquired after January 19, 2025. Used together, most kitchen equipment purchases can be fully expensed in the year placed in service.

What is the depreciation life of commercial kitchen equipment?

Under MACRS GDS, commercial kitchen equipment (ovens, refrigerators, fryers, dishwashers) generally falls in the 5-year property class under Asset Class 57.0. Physical operational life typically runs 10–15 years, so tax life and actual useful life diverge considerably.

Do restaurant improvements qualify for bonus depreciation?

Qualified improvement property (QIP)—interior improvements to a nonresidential building placed in service after the building's original placed-in-service date—has a 15-year GDS recovery period and qualifies for bonus depreciation. Restaurant remodels, kitchen upgrades, and interior renovations frequently meet the QIP definition.

What is the difference between Section 179 and bonus depreciation for restaurant equipment?

Section 179 is capped at $2,500,000 annually and requires active business income to avoid a net operating loss, while bonus depreciation has no dollar cap and can produce a loss on both new and used qualifying property. In practice, Section 179 applies first, then bonus depreciation covers the remainder.