Default straight-line depreciation treats your rental property as a single slow-depreciating asset — spreading deductions evenly over 27.5 years for residential property or 39 years for commercial. That math works fine for the IRS. It doesn't work well for your cash flow. A property with a $900,000 cost basis generates just $32,727 per year under straight-line. With cost segregation and bonus depreciation applied correctly, that same property can generate over $174,000 in first-year deductions.

The gap between those numbers isn't a loophole. It's the difference between defaulting to a slow system and actively using the accelerated methods embedded in the federal tax code under IRC Section 168 — methods the IRS explicitly sanctions and publishes guidance on.

This article covers how tax drag builds under default depreciation, what determines your acceleration potential, which methods apply to which assets, and the strategies that extract the most value — from method selection to cost segregation timing and depreciation recapture planning.

Key Takeaways

- Straight-line depreciation spreads deductions evenly over 27.5 years (residential) or 39 years (commercial) — leaving significant deductions unclaimed in the early years of ownership

- Qualifying components — appliances, flooring, landscaping, and more — can be depreciated over 5, 7, or 15 years instead, front-loading your deductions

- Bonus depreciation is now permanently restored to 100% for qualifying property placed in service after January 19, 2025 under the One Big Beautiful Bill Act

- A cost segregation study is the most reliable way to identify qualifying components — and look-back studies let you reclaim missed deductions on properties you've owned for years

- Accelerated depreciation defers taxes — it doesn't eliminate them. Recapture planning is essential before you sell

How Landlords Quietly Overpay in Taxes Year After Year

How Landlords Consistently Overpay in Taxes Year After Year

Default straight-line depreciation is legal and IRS-approved. It's also one of the most expensive habits a landlord can have.

Under the standard approach, every year you own a residential rental, you claim the same modest deduction. The bulk of a property's depreciable value sits unclaimed during the early years of ownership. That's a problem, because those early years are typically when landlords carry the highest income and the greatest need for tax relief.

The "Allowed or Allowable" Problem

Here's what most landlords don't realize: the IRS adjusts your cost basis for depreciation you were entitled to claim — whether you actually claimed it or not.

This is the "allowed or allowable" rule under IRC Section 1016(a)(2). If you never claimed depreciation on a rental property, the IRS still assumes you did when you sell. You'll owe recapture taxes on deductions you never took. You lose twice — no annual savings during ownership, and full recapture liability at exit.

The Compounding Cost of Under-Deducting

The tax drag from default depreciation isn't a single visible event. Each year a landlord under-deducts:

- More taxes paid than necessary

- Less capital available to reinvest or renovate

- Reduced ability to acquire additional properties

- Lost time value on deferred savings

The IRS permits faster depreciation for specific property components, but only if the landlord proactively identifies and claims them. That's not something the default system — or most tax software — will flag on its own.

Key Factors That Determine Your Accelerated Depreciation Potential

Not every property offers the same acceleration opportunity. The magnitude of what you can front-load depends on several interconnected factors.

Property Composition

The most important variable is how much of your purchase price can be attributed to shorter-lived components — 5-year, 7-year, and 15-year assets — versus the building structure itself.

Based on Seneca Cost Segregation's work across more than 10,200 properties, reclassification rates vary significantly by property type:

| Property Type | Typical Reclassification Rate |

|---|---|

| Mobile home parks | 80–85% |

| Medical facilities / banks | 25–43% |

| Hotels / hospitality | 25–40% |

| Restaurants | 23–40% |

| Self-storage | 30–35% |

| Multifamily residential | 15–25% |

| Basic warehouses / industrial | 10–17% |

Properties with more personal property and land improvements — parking lots, landscaping, appliances, specialized systems — tend to offer greater acceleration potential.

Your Tax Situation

Whether you can actually use accelerated deductions depends on three factors:

- Income level — The same $100,000 in additional depreciation generates $24,000 in tax savings at the 24% bracket versus $37,000 at the 37% bracket

- Active vs. passive participation — Passive activity rules under IRC Section 469 limit how rental losses offset other income

- Real estate professional status — Landlords who qualify (750+ hours/year in real property trades) can use losses without limitation; active participants may deduct up to $25,000 in passive rental losses against ordinary income, subject to phase-out between $100,000–$150,000 AGI

- Suspended losses — If your rental activity is passive and your income exceeds the phase-out threshold, accelerated deductions may accumulate as deferred losses until you sell

Your CPA can model which scenario applies to you before you commit to a cost segregation study.

Accelerated Depreciation Methods for Landlords

Several IRS-sanctioned methods are available. The right choice depends on the asset type, holding period, and your overall tax position.

Straight-Line vs. Accelerated: The Core Distinction

Straight-line depreciation treats the property as a single asset and spreads deductions evenly across 27.5 or 39 years. Accelerated methods disaggregate the property into individual components and apply faster depreciation schedules to those with shorter useful lives.

That difference in treatment — one slow asset versus many faster-depreciating components — is what drives the tax benefit in each method below.

Double-Declining Balance (DDB) Method

DDB doubles the straight-line rate and applies it to the remaining book value each year. For a 5-year asset, the straight-line rate is 20%, so DDB applies 40% annually on declining value — front-loading deductions heavily in years one through three.

This method works best for assets that lose value quickly: appliances, computers, certain fixtures. It doesn't apply to the building structure itself, which remains on the 27.5 or 39-year straight-line schedule.

Sum-of-the-Years' Digits (SYD) Method

SYD assigns a declining fraction of depreciation to each year based on remaining useful life. For a 5-year asset, the denominator is 15 (1+2+3+4+5), so Year 1 gets 5/15 of the depreciable basis, Year 2 gets 4/15, and so on.

Deductions taper more gradually than DDB, making SYD better suited for assets expected to hold value longer before replacement. SYD is codified under Section 167, not standard MACRS — it's not the default method for rental property placed in service after 1986.

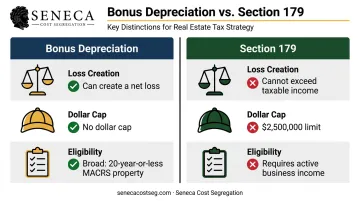

Bonus Depreciation and Section 179

Bonus depreciation is the most powerful option for most landlords. Qualifying property — assets with a useful life of 20 years or less — can be deducted 100% in the year placed in service.

The One Big Beautiful Bill Act (Public Law 119-21, signed July 4, 2025) permanently restored 100% bonus depreciation for qualifying property acquired and placed in service after January 19, 2025. This eliminates the phase-down schedule that had been reducing the deduction percentage under prior law.

Section 179 operates differently. It allows immediate expensing up to $2,500,000 for taxable years beginning after December 31, 2024, but carries a critical limitation for landlords: it generally requires the rental activity to qualify as an active trade or business under IRC Section 179(b)(3). Most passive rental investors cannot use Section 179 without additional structuring — verify with a tax professional before assuming eligibility.

Key distinction between the two:

- Bonus depreciation can create or increase a net loss; Section 179 cannot

- Bonus depreciation has no dollar cap; Section 179 has an annual limit

- Bonus depreciation applies broadly to 20-year-or-less MACRS property; Section 179 requires active business income to absorb the deduction

Strategies to Maximize Accelerated Depreciation Benefits

Selecting the right method is only the start. These strategies address how landlords can change decisions, documentation practices, and their investment context to extract the most value.

Time Your Cost Segregation Study Correctly

Order a study before filing your first return on a newly acquired property. Completing the study in the same year of purchase, renovation, or construction maximizes first-year deductions without requiring a Form 3115 change in accounting method.

For properties with planned renovations, wait until improvements are complete — this avoids paying for two separate studies and ensures all costs are captured in one comprehensive analysis.

Use Look-Back Studies for Properties You've Owned for Years

If you've owned income-producing property without a cost segregation study, you haven't necessarily missed the window. IRS rules via Rev. Proc. 2015-14 allow landlords to claim cumulative missed deductions through a Form 3115 (Change in Accounting Method) filing — without amending prior returns.

MACRS look-back studies apply to properties placed in service as early as January 1, 1987. The catch-up deduction is claimed in a single tax year. Seneca's look-back studies include Form 3115 preparation as a standard deliverable at no additional charge.

Properties older than 10 years may offer diminishing returns on study costs — run the numbers before ordering a study.

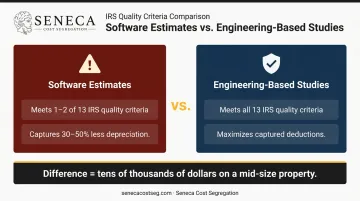

Commission an Engineering-Based Study

Not all cost segregation studies are equal. The IRS Cost Segregation Audit Techniques Guide (Pub. 5653) identifies the detailed engineering approach from actual cost records as the most methodical and accurate method — and describes quality studies as requiring expertise, documentation, site inspections, cost allocation, and asset classification.

Software estimates typically satisfy 1–2 of the IRS's quality criteria. Engineering-based studies meet all 13. The difference in captured deductions can be substantial: software tools capture 30–50% less depreciation than engineering-based approaches, representing tens of thousands of dollars in missed deductions on a mid-size property.

Seneca Cost Segregation's engineering team has completed over 10,200 studies nationwide, delivering an average first-year deduction of $171,243.

Every study includes separate asset-class depreciation schedules (5-year, 7-year, 15-year, and 27.5/39-year), cost reconciliation workpapers, CPA implementation support, and AuditDefense with a money-back guarantee. If an audit results in more than a 5% adjustment attributable to Seneca's work, the study fee is refunded in full.

Elect Bonus Depreciation Strategically

Bonus depreciation is most valuable in high-income years when you have significant taxable income to offset. In low-income years, the deduction may generate suspended losses that don't produce current tax savings.

Before accelerating aggressively, consider:

- Properties sold within 3–5 years face depreciation recapture that can offset much of the benefit

- A 1031 exchange defers recapture indefinitely; a straight sale triggers it immediately

- Passive losses from accelerated depreciation may be suspended if you don't meet active participation or REP status thresholds

Qualify as a Real Estate Professional or Use the Active Participation Exception

Passive activity rules under IRC Section 469 are where accelerated depreciation loses its power for many landlords. Two pathways preserve it:

- Active participation exception: Deduct up to $25,000 in passive rental losses against ordinary income (phases out between $100,000–$150,000 AGI)

- Real estate professional status: 750+ hours per year in real property trades or businesses, with real estate comprising more than 50% of personal services — eliminates the passive limitation entirely

Short-term rental operators (average guest stay of 7 days or fewer) who meet material participation tests may also reclassify rental income as active, unlocking the ability to use depreciation losses against W-2 and business income.

What to Watch Out For: Depreciation Recapture and Common Pitfalls

Accelerated depreciation defers taxes — it doesn't make them disappear.

How Depreciation Recapture Works

When you sell a rental property, the IRS recaptures previously depreciated amounts:

- Section 1250 property (buildings, 15-year improvements) — taxed at a maximum 25% rate as unrecaptured Section 1250 gain

- Section 1245 property (personal property like appliances, flooring) — taxed at ordinary income rates up to 37%

- High-income investors may also owe 3.8% Net Investment Income Tax on top of recapture rates

Aggressive acceleration increases the total amount subject to recapture. The more you front-load, the larger the potential bill at sale — unless you plan around it.

One effective planning tool: rolling proceeds into a like-kind replacement property under IRC Section 1031 defers recapture indefinitely. Each successive exchange resets the clock, keeping your capital working rather than going to the IRS.

Understanding recapture mechanics is half the battle. The other half is avoiding the execution errors that cost landlords real money.

Common Mistakes to Avoid

- Skipping cost segregation entirely still leaves you owing recapture on deductions you never took — the IRS's allowed-or-allowable rule applies regardless

- Depreciating land, which is never permitted — land doesn't wear out and cannot be depreciated under any method

- Front-loading bonus depreciation in a low-income year, where the deduction produces minimal benefit and the acceleration is effectively wasted

- Ignoring recapture exposure when planning a sale, which is especially costly on short-term holds

- Lumping component values into a single depreciation line, which forfeits faster schedules and flags audit risk

State Tax Non-Conformity

Federal bonus depreciation doesn't automatically translate to your state return. Several states — including California, New York, New Jersey, Minnesota, and South Carolina — decouple from federal bonus depreciation rules, requiring separate state depreciation calculations and requiring add-backs on state returns.

The Tax Foundation's 2025 analysis found that only 15 states offer Section 168(k) first-year expensing to the same degree as the federal government. Verify your state's treatment with a tax professional before projecting total tax savings.

Conclusion

Accelerated depreciation is a legitimate, IRS-sanctioned strategy — one that lets landlords time deductions strategically, recover investment costs sooner, and redirect more cash into the next deal.

The strategy delivers its full value only with proper documentation, the right depreciation method for each asset class, and coordinated planning around passive activity rules, recapture exposure, and your broader tax picture. A cost segregation study is typically the most direct way to identify which components qualify for accelerated treatment — and to capture deductions you may have already left on the table.

Frequently Asked Questions

What is accelerated depreciation for real estate?

Accelerated depreciation is an IRS-permitted method that lets landlords front-load deductions on qualifying property components — appliances, flooring, land improvements — over 5, 7, or 15 years instead of the standard 27.5- or 39-year building life. This reduces taxable income faster in the early years of ownership, improving after-tax cash flow when reinvestment opportunities are highest.

What real estate assets qualify for accelerated depreciation?

Common qualifying assets include appliances, carpeting, vinyl flooring, decorative lighting, cabinetry, window treatments, landscaping, irrigation systems, fencing, driveways, parking lots, patios, and certain HVAC components. Land itself and the building's core structural components do not qualify. A cost segregation study is the most reliable way to identify and document all eligible components.

Do you have to pay back accelerated depreciation when you sell real estate?

Not directly, but the IRS taxes depreciation recapture at sale. Section 1250 gain (buildings and 15-year improvements) is taxed at a maximum 25% rate; Section 1245 property (personal property) is recaptured at ordinary income rates up to 37%. A 1031 exchange can defer this liability indefinitely by rolling proceeds into a like-kind replacement property.

What is the difference between bonus depreciation and Section 179 for landlords?

Bonus depreciation — now at 100% for qualifying property placed in service after January 19, 2025 — applies to assets with a 20-year-or-less useful life and carries no dollar cap. Section 179 allows immediate expensing up to $2,500,000 but requires the rental activity to qualify as an active trade or business, which most passive rental investors cannot satisfy without additional structuring.

How does a cost segregation study help landlords claim accelerated depreciation?

A cost segregation study is an engineering-based analysis that breaks a property into individual components, assigns each the correct IRS depreciation class, and produces audit-ready documentation for every deduction claimed. This identifies far more accelerated depreciation than a landlord would find independently and ensures the deductions hold up under IRS review.

Can landlords use accelerated depreciation on properties they've already owned for years?

Yes. Look-back cost segregation studies allow landlords to claim cumulative missed deductions for properties placed in service as early as January 1, 1987. You claim the catch-up amount in a single tax year via Form 3115 — no amended prior returns required. Seneca includes Form 3115 preparation as a standard deliverable in all look-back studies.